Have you ever stopped to wonder why in 2008 all of Wall Street pretty much failed? Why not in 1973 during the Arab Oil Embargo? Why not in 1987 after the crash? The Dow dropped 28% on black Monday - 52% that quarter, but only EF Hutton failed.

Did you know that FASB 157 went into effect November 15, 2007? Interesting........

Did you know that FASB 157 went into effect November 15, 2007? Interesting........

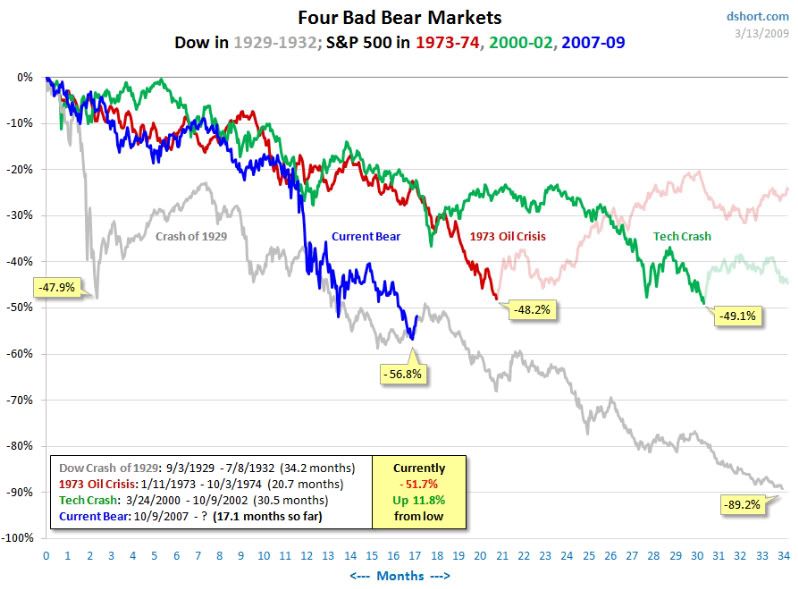

As evidenced by the chart, we have been here before, albeit for all different reasons. In the 1973-1974 downturn the trigger was the Arab Oil Embargo. The contraction of 2000-2002 was prolonged by 9-11. The current collapse has been frequently compared to the Great Depression. History will one day show that both may have been born of the same mother. Mark-to-market accounting rules caused banks to fail in the Great Depression, not from bad loans, but from writing down values at the behest of regulators. FDR eventually called together his economic panel in 1938 and suspended those rules. By then the Depression had lasted eight years, despite public works (WPA) and large spend projects like the Hoover Dam.

At the epicenter of the current storm, mark-to-market a/k/a "fair value" accounting once again is center stage. The principles of fair value--also known as "mark-to-market"--accounting are described in the Statement of Financial Accounting Standards (SFAS) No. 157, which was adopted by FASB in 2006 for use after Nov. 15, 2007. Fair value measurements rely on exchange prices between market participants in orderly transactions. The system replaces historical cost accounting, which had been standard since 1938. The previous version required preparers to book assets at their original cost, and to mark them down where they deemed a permanent impairment--but never to mark them up.

At the epicenter of the current storm, mark-to-market a/k/a "fair value" accounting once again is center stage. The principles of fair value--also known as "mark-to-market"--accounting are described in the Statement of Financial Accounting Standards (SFAS) No. 157, which was adopted by FASB in 2006 for use after Nov. 15, 2007. Fair value measurements rely on exchange prices between market participants in orderly transactions. The system replaces historical cost accounting, which had been standard since 1938. The previous version required preparers to book assets at their original cost, and to mark them down where they deemed a permanent impairment--but never to mark them up.

When SFAS No. 157 was first adopted, about a year before the meltdown, it was considered relatively uncontroversial. Lawmakers, regulators and the financial sector blame fair value rules for the destruction of banks' balance sheets, while opposing forces maintain that marking to market helps protect investors by reflecting economic conditions, harsh as they may be. After all, the overarching purpose of accounting is to provide useful information that is reliable and relevant to decision makers. William Isaac, chairman of the FDIC from 1981 to 1985, has been a vocal champion for returning to historical cost. He argues we had a perfectly good working system before they decided to impose this grand experiment. He cites a suite of correspondence in the early 1990s from Alan Greenspan, then-Secretary of the Treasury Nicholas Brady, and Bill Taylor, chairman of the FDIC, all expressing alarm that market value accounting could lead to misleading and volatile bank earnings. It could even result in "more intense and frequent credit crunches, since a temporary dip in asset prices would result in immediate reductions in bank capital and an inevitable retrenchment in bank lending capacity," Brady wrote to the FASB on March 24, 1992 . Sixteen years, later, that is exactly what happened as evidenced by the destruction of hundreds of billions of bank capital.

Depending on the intention, there are different ways to hold financial instruments. Are they to be sold, traded or retained? Fair value does not apply to those assets held to maturity rather than in trading accounts. Suppose a bank has issued a loan to a real estate developer. Even if the development is in trouble, as long as the bank intends to hold the loan to maturity and has the ability to do so, it does not have to mark it down at all unless the asset has been impaired, showing some evidence like a missed interest payment. It makes sense that banks or insurance companies should carry loans at book, rather than market value, as long as borrowers are making interest payments.

When the rules took effect last year, no one foresaw the unprecedented volatility to come. Some liquid stocks, like General Electric, have seen their share prices halved; most people would concede to an assumption that its price was fair a year ago, and is still fair today. Other securities, like the ABX index, which is composed of the longest duration, highest risk sub prime issues, have been disproportionately hammered.

Still other markets have simply dried up as buyers retreated en masse, leaving no quoted prices in active trading, or else gargantuan spread prices that reflect abnormal conditions. Many of the securities being marked down now are illiquid. Distressed or forced liquidation sales are generally not orderly, whereas some securities were never intended for sale at all. I believe that there will be a return to cash accounting and that will end the destruction of bank capital. That will also mark the end to the Great Panic of 2008. We are awash in a sea of opportunity with valuations seen once in a generation. If my thesis is correct and mark to market is the root cause of the systemic collapse of the shadow banking system, then the suspension, removal or revision of FASB 157 will usher in a period of material reflation. We will once again return to normalcy.