I'm always trying to find interesting information that will allow you to make intelligent decisions. Last weekend I spent several hours reading various publications and thought I would share some interesting information coming from Business Week magazine.

As you read the comments, you can see how various aspects of the economic recovery plan are being challenged by businesses.

What the White House wants: Emissions

To cut emissions that cause global warming, the Administration proposes a "tap and trade" system. This would require companies to pay $646 billion over eight years to buy the tradable rights to emit such pollutants. Much of the money would be returned to consumers.

What business thinks:

Many companies do not oppose a price tag on carbon emissions, since it provides more certainty and boosts investments in efficiency and renewable energy. But they worry that selling all of the permits from the start can impose a huge burden on the companies involved.

What the White House wants: Healthcare

The President has provided $634 billion in the proposed budget to help pay for health care reforms over the next 10 years. Half that some will come from tax hikes and half from cuts in Medicare payments to insurers, drug companies and hospitals.

What business thinks:

On the surface, business broadly backs health care reform. But the cracks are starting to show: insurers fear competition from government-backed rivals, hospitals worry costs will be squeezed, and drugmakers face far lower prices.

What the White House wants: Foreign Tax

Multinationals currently can defer US taxes on profits earned abroad until they bring the funds back home. The Administration says that encourages companies to ship jobs overseas. It plans to raise $210 billion by limiting the tax deferral and other overseas breaks.

What business thinks:

Companies fear they will be at a competitive disadvantage if they have to pay US rates on foreign operations while their rivals pay lower local rates. Any loss of revenues overseas, they add, will result in US jobs lost, not gained.

What the White House wants: Income Tax

The President would boost the top rates for families making more than $250,000 from 33% to 36%; those earning over $370,000 would go to 39.6%. Capital gains and dividends rate would rise from 15% to 20%. Deductions for mortgage interest and charitable giving drops to 28%.

What business thinks:

Fears that tax hikes will discourage the well-off from investing are shared by a host of businesses, from homebuilders and mortgage brokers desperate for a housing rebound to mutual fund companies and other investment managers struggling to keep investors in the market.

What the White House wants: Drilling

Converting the economy to cleaner energy has emerged as one of the Administration's top goals. If it has its way, that means an end to a host of tax breaks for oil and gas producers, including tax credits aimed at spurring domestic offshore drilling.

What business thinks:

The oil industry plans to mount a fierce fight to keep its tax perks, arguing that the President's plan puts jobs and energy security at risk. Plus, making drilling more expensive in the US could encourage oil giants to shift even more investment in exploration abroad.

What the White House wants: Agriculture

The President wants to end what he considers wasteful agricultural subsidies. He is counting on saving $9.8 billion over 10 years by capping payments at $250,000 annually to farmers whose gross sales do not exceed $500,000 a year.

What business thinks:

The agricultural lobby, which spent $131 million in lobbying in 2008, is among the fiercest defenders of turf in Washington. It will argue that farmers can't stay in business, especially in a tough economy, without support for cotton,

rice, and other crops.

It seems to me that the battle lines are being drawn. I believe the recovery of this economy is going to require give-and-take on both sides. As we learn more about the details I will share some more thoughts with you.

Bill Spiropoulos

President & CEO

CoreStates Capital Advisors

Wednesday, April 1, 2009

Sunday, March 1, 2009

Avoid Being Scammed by your Advisor!

Ponzi schemes, front running, self-dealing, churning and outright fraud are just a few of the multitude of ways you can be cheated by your financial advisor. Protect yourself by following these eight practical guidelines.

1. Understand your Advisory Agreement

Be sure your Advisory Agreement describes the services you want, and that your advisor bears fiduciary responsibility to provide them. Don't have an Advisory Agreement? Demand one from your advisor!

2. Insist on a Personalized Investment Policy Statement

A personalized Investment Policy Statement assures that your expectations and the expectations of your manager are in snyc regarding the management of your account.

3. Specify Asset-Based Fees

Your management fee should increase only if the value of your account increases, and should decline if your account declines.

4. Require an Independent Custodian & Accountant

Your advisor should have management discretion, but not custody of your assets or control of your statement preparation.

5. Monitor Manager & Subadvisor Audits

Independently prepared financial statements and regulatory reviews should verify the advisor's and all managers' financial health and regulatory compliance.

6. Have (and use!) 24/7 Online Account Access

"Trust, but verify" that all activities in your account reflect your objectives and Investment Policy Statement.

7. Meet Regularly with Your Advisor

The better you know each other, the better your needs, goals, and expectations will be met.

8. If it sounds too good ...

Stop and think. It's highly likely that the advisor who makes rash promises or claims a record of unusually high or consistent returns will soon have Madoff with your money!

1. Understand your Advisory Agreement

Be sure your Advisory Agreement describes the services you want, and that your advisor bears fiduciary responsibility to provide them. Don't have an Advisory Agreement? Demand one from your advisor!

2. Insist on a Personalized Investment Policy Statement

A personalized Investment Policy Statement assures that your expectations and the expectations of your manager are in snyc regarding the management of your account.

3. Specify Asset-Based Fees

Your management fee should increase only if the value of your account increases, and should decline if your account declines.

4. Require an Independent Custodian & Accountant

Your advisor should have management discretion, but not custody of your assets or control of your statement preparation.

5. Monitor Manager & Subadvisor Audits

Independently prepared financial statements and regulatory reviews should verify the advisor's and all managers' financial health and regulatory compliance.

6. Have (and use!) 24/7 Online Account Access

"Trust, but verify" that all activities in your account reflect your objectives and Investment Policy Statement.

7. Meet Regularly with Your Advisor

The better you know each other, the better your needs, goals, and expectations will be met.

8. If it sounds too good ...

Stop and think. It's highly likely that the advisor who makes rash promises or claims a record of unusually high or consistent returns will soon have Madoff with your money!

Friday, February 13, 2009

Mark-to-Market Accounting

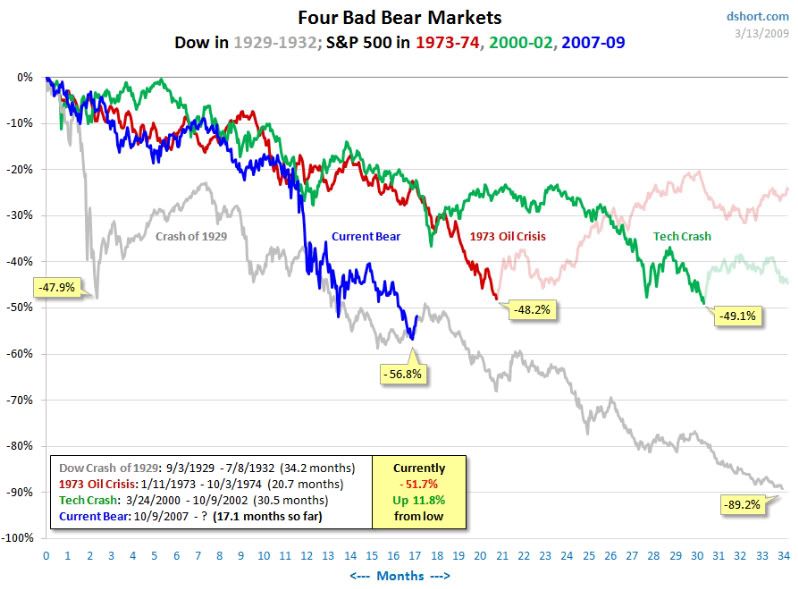

Have you ever stopped to wonder why in 2008 all of Wall Street pretty much failed? Why not in 1973 during the Arab Oil Embargo? Why not in 1987 after the crash? The Dow dropped 28% on black Monday - 52% that quarter, but only EF Hutton failed.

Did you know that FASB 157 went into effect November 15, 2007? Interesting........

Did you know that FASB 157 went into effect November 15, 2007? Interesting........

As evidenced by the chart, we have been here before, albeit for all different reasons. In the 1973-1974 downturn the trigger was the Arab Oil Embargo. The contraction of 2000-2002 was prolonged by 9-11. The current collapse has been frequently compared to the Great Depression. History will one day show that both may have been born of the same mother. Mark-to-market accounting rules caused banks to fail in the Great Depression, not from bad loans, but from writing down values at the behest of regulators. FDR eventually called together his economic panel in 1938 and suspended those rules. By then the Depression had lasted eight years, despite public works (WPA) and large spend projects like the Hoover Dam.

At the epicenter of the current storm, mark-to-market a/k/a "fair value" accounting once again is center stage. The principles of fair value--also known as "mark-to-market"--accounting are described in the Statement of Financial Accounting Standards (SFAS) No. 157, which was adopted by FASB in 2006 for use after Nov. 15, 2007. Fair value measurements rely on exchange prices between market participants in orderly transactions. The system replaces historical cost accounting, which had been standard since 1938. The previous version required preparers to book assets at their original cost, and to mark them down where they deemed a permanent impairment--but never to mark them up.

At the epicenter of the current storm, mark-to-market a/k/a "fair value" accounting once again is center stage. The principles of fair value--also known as "mark-to-market"--accounting are described in the Statement of Financial Accounting Standards (SFAS) No. 157, which was adopted by FASB in 2006 for use after Nov. 15, 2007. Fair value measurements rely on exchange prices between market participants in orderly transactions. The system replaces historical cost accounting, which had been standard since 1938. The previous version required preparers to book assets at their original cost, and to mark them down where they deemed a permanent impairment--but never to mark them up.

When SFAS No. 157 was first adopted, about a year before the meltdown, it was considered relatively uncontroversial. Lawmakers, regulators and the financial sector blame fair value rules for the destruction of banks' balance sheets, while opposing forces maintain that marking to market helps protect investors by reflecting economic conditions, harsh as they may be. After all, the overarching purpose of accounting is to provide useful information that is reliable and relevant to decision makers. William Isaac, chairman of the FDIC from 1981 to 1985, has been a vocal champion for returning to historical cost. He argues we had a perfectly good working system before they decided to impose this grand experiment. He cites a suite of correspondence in the early 1990s from Alan Greenspan, then-Secretary of the Treasury Nicholas Brady, and Bill Taylor, chairman of the FDIC, all expressing alarm that market value accounting could lead to misleading and volatile bank earnings. It could even result in "more intense and frequent credit crunches, since a temporary dip in asset prices would result in immediate reductions in bank capital and an inevitable retrenchment in bank lending capacity," Brady wrote to the FASB on March 24, 1992 . Sixteen years, later, that is exactly what happened as evidenced by the destruction of hundreds of billions of bank capital.

Depending on the intention, there are different ways to hold financial instruments. Are they to be sold, traded or retained? Fair value does not apply to those assets held to maturity rather than in trading accounts. Suppose a bank has issued a loan to a real estate developer. Even if the development is in trouble, as long as the bank intends to hold the loan to maturity and has the ability to do so, it does not have to mark it down at all unless the asset has been impaired, showing some evidence like a missed interest payment. It makes sense that banks or insurance companies should carry loans at book, rather than market value, as long as borrowers are making interest payments.

When the rules took effect last year, no one foresaw the unprecedented volatility to come. Some liquid stocks, like General Electric, have seen their share prices halved; most people would concede to an assumption that its price was fair a year ago, and is still fair today. Other securities, like the ABX index, which is composed of the longest duration, highest risk sub prime issues, have been disproportionately hammered.

Still other markets have simply dried up as buyers retreated en masse, leaving no quoted prices in active trading, or else gargantuan spread prices that reflect abnormal conditions. Many of the securities being marked down now are illiquid. Distressed or forced liquidation sales are generally not orderly, whereas some securities were never intended for sale at all. I believe that there will be a return to cash accounting and that will end the destruction of bank capital. That will also mark the end to the Great Panic of 2008. We are awash in a sea of opportunity with valuations seen once in a generation. If my thesis is correct and mark to market is the root cause of the systemic collapse of the shadow banking system, then the suspension, removal or revision of FASB 157 will usher in a period of material reflation. We will once again return to normalcy.

Sunday, February 1, 2009

Who Can you Trust?

Once again, greed has rocked the foundation of our financial system. It has led to dishonesty, outright theft, and pervasive emotional detachment, and has caused each of us to question every financial relationship we have.

Our trust in our financial institutions is gone.We have been deceived by Freddie Mac, Fannie Mae, Congress, the SEC, AIG, Citigroup, and most recently Bernard Madoff. Each of these, in its own way, has shown that the further away from the investor an institution is, the greater the emotional detachment,and the easier it is for the institution to betray its clients' trust.

In this environment, "transparency" becomes critically important. The literal derivation of "transparent" is "able to see through." In financial relationships, it means the ability of the client to actually see the activities their financial services provider is undertaking on their behalf.

We have established and structured CoreStates to have multiple checks and balances that insure complete transparency. We have leading independent custodians safeguarding our clients' assets. We require our managers to have certified independent audits and peer reviews. An unaffiliated third party conducts the accounting for our clients' assets and generates the account statements that are provided directly from them to our clients. And, our clients maintain total 24/7 access to their account statements online. In other words, our clients are "able to see through" to each and every action taken in their accounts.

What that means to us at CoreStates is that everything we do and every decision we make is visible to our clients, and must be in their best interests.

That commitment to always act in our clients' best interests is what makes us a fiduciary. By law, fiduciaries are required to act in the best interests of the investor. We are held to a higher standard than are brokerage firms' registered representatives. We are the stewards of our clients' wealth. We ask our clients to be Serious Investors, and we demand that we be Serious Advisors.

Great companies, just like great people, are guided by a core set of values that provide a foundation for their beliefs and their behavior. The following are CoreStates' CoreValues. They have been guiding our conduct since the very beginning of CoreStates.

- We value lifetime client relationships.

- We value the family, respecting its long-term generational needs.

- We value honesty and integrity, the cornerstones of business and personal relationships.

- We value the power of transparent communication, the catalyst for trust.

- We value teamwork, the collaboration of individual initiatives and opinions.

- We value quality, if it's worth doing, it's worth doing right.

- We value education, the foundation for a lifetime of personal growth.

- We value the impact of partnerships, the blending of professional skills to solve client problems.

- We value extraordinary service, viewing what we do through the eyes of the client.

- We value diverse opinions, the foundation for the best investment decisions.

We realize that each and every one of our clients is guided by their own personal values. Over the past 30 years we have gotten to know and respect those guiding principles. The ideal financial relationship is a collaboration of like-minded people

guided by common values and objectives. As we move forward through 2009, I invite you to become more involved with every aspect of CoreStates. We have created one

of the industry's most instructive websites at www.corestates.us. We are proud of our efforts to keep clients informed, in touch and feeling secure about their

investments and their relationship with CoreStates.

Our trust in our financial institutions is gone.We have been deceived by Freddie Mac, Fannie Mae, Congress, the SEC, AIG, Citigroup, and most recently Bernard Madoff. Each of these, in its own way, has shown that the further away from the investor an institution is, the greater the emotional detachment,and the easier it is for the institution to betray its clients' trust.

In this environment, "transparency" becomes critically important. The literal derivation of "transparent" is "able to see through." In financial relationships, it means the ability of the client to actually see the activities their financial services provider is undertaking on their behalf.

We have established and structured CoreStates to have multiple checks and balances that insure complete transparency. We have leading independent custodians safeguarding our clients' assets. We require our managers to have certified independent audits and peer reviews. An unaffiliated third party conducts the accounting for our clients' assets and generates the account statements that are provided directly from them to our clients. And, our clients maintain total 24/7 access to their account statements online. In other words, our clients are "able to see through" to each and every action taken in their accounts.

What that means to us at CoreStates is that everything we do and every decision we make is visible to our clients, and must be in their best interests.

That commitment to always act in our clients' best interests is what makes us a fiduciary. By law, fiduciaries are required to act in the best interests of the investor. We are held to a higher standard than are brokerage firms' registered representatives. We are the stewards of our clients' wealth. We ask our clients to be Serious Investors, and we demand that we be Serious Advisors.

Great companies, just like great people, are guided by a core set of values that provide a foundation for their beliefs and their behavior. The following are CoreStates' CoreValues. They have been guiding our conduct since the very beginning of CoreStates.

- We value lifetime client relationships.

- We value the family, respecting its long-term generational needs.

- We value honesty and integrity, the cornerstones of business and personal relationships.

- We value the power of transparent communication, the catalyst for trust.

- We value teamwork, the collaboration of individual initiatives and opinions.

- We value quality, if it's worth doing, it's worth doing right.

- We value education, the foundation for a lifetime of personal growth.

- We value the impact of partnerships, the blending of professional skills to solve client problems.

- We value extraordinary service, viewing what we do through the eyes of the client.

- We value diverse opinions, the foundation for the best investment decisions.

We realize that each and every one of our clients is guided by their own personal values. Over the past 30 years we have gotten to know and respect those guiding principles. The ideal financial relationship is a collaboration of like-minded people

guided by common values and objectives. As we move forward through 2009, I invite you to become more involved with every aspect of CoreStates. We have created one

of the industry's most instructive websites at www.corestates.us. We are proud of our efforts to keep clients informed, in touch and feeling secure about their

investments and their relationship with CoreStates.

Tuesday, January 27, 2009

Thursday, January 1, 2009

2009 Outlook

2009 Outlook The Bottom LineAt CoreStates remain positive about the ability of the U. S. and international investment markets to provide patient investors with favorable, inflation-beating, long-term returns. But, we also believe the changing priorities of our government and of other administrations worldwide can make our future economic prospects decidedly less favorable than they have been. The following points highlight what we see for 2009 in the major areas pertinent to investors.

Economy – The global downturn will continue, and is likely to worsen through 2009 and possibly much longer as governments and financial institutions worldwide attempt to limit its severity at the expense of extending its duration. U. S. unemployment will rise well above 7% and production will decline markedly as businesses attempt to align their output with shrinking demand.

Inflation – The widespread actions of governments and financial institutions to support over-extended borrowers with additional borrowings will eventually foster inflation. But, through 2009 at least, it will be moderated by the deflationary effects of the downturn.

Bond markets – Fixed income investors will be increasingly tempted by these government and corporate actions to focus not on the financial health and economic prospects of issuers, but on their perceived economic importance and political strength. It will encourage increased risk-taking by sophisticated, unregulated investors, while driving other investors further into the lowest risk, lowest potential return investments.

Global stock markets – Equities will remain extremely volatile as investors’ hopes for economic recovery are periodically inflated then dashed by economic reports, geopolitical events, and governmental actions. We expect disappointments and new areas of concern to exceed positive surprises, leading to further stock market declines before year-end.

Real Estate – Weakness will moderate in both commercial and residential markets as governmental efforts to increase demand and dampen the growing supply of properties for sale.

Energy and Materials – Efforts by producing nations to curtail output will put a floor under prices, but will be insufficient to push prices sharply higher in the face of continued recession-related declines in global demand this year.

Agricultural commodities – Demand growth in developing economies will continue to support prices in all areas other than current biofuel crops where the accelerating development of alternative biofuel sources is likely to depress prices.

Precious Metals – Weakness in industrial demand will be more than offset by investors’ increasing desire for safe, universally honored, “hard” assets.

Currencies – Efforts by investors and commercial users of the currency markets to discern the relative prospects for the G8 and developing economies will keep these markets volatile week-to-week and month-to-month, but largely trendless from the beginning to the end of 2009. We believe the U.S. Dollar will remain stable during the global crisis and economic downturn. The Dollar remains the reserve currency of choice for now.

External Market Influences – Difficult economic conditions around the globe coupled with a new administration in Washington and a plethora of geopolitical confrontations are certain to produce worrisome incidents throughout the year. Investment markets will react accordingly, with risk premiums remaining high and the lowest risk investments moving to even higher valuations.

Our Recommendations:

Diversification, which provided only limited protection in 2008, will be more important in 2009. We expect the greatest success with “bar bell” allocations – those consisting primarily of some very safe, highly liquid investments together with a modest but growing exposure to carefully selected higher risk assets. This mix, if well managed, should provide returns significantly in excess of a portfolio of all asset classes equally weighted.

Trading will become more important in the volatile but range-bound markets we expect. Buy-and-hold returns in most asset classes will be largely disappointing.

Patience will be required throughout the year, although limited market rallies will provide occasional encouragement.

Volatile but generally trendless markets (as described) appear most likely, but the precarious nature of global economies and geopolitics creates the possibility of sudden large moves in either direction reaching extreme levels that could persist for an extended period. So, although we never expect to fully capture any such surprise moves, we will remain vigilant and ready to reallocate our portfolios as we deem prudent in response to the expected rapidly changing environment.

CoreStates Strategies:

The best long-term investment purchases are made when others are selling, when fear is greatest, when the outlook is most bleak. The current environment certainly fits this description. But, we expect this gloom to gradually (though erratically) dissipate over the next several quarters. We intend to capitalize on this by carefully managing but generally retaining our current allocations, but also doing some strategic buying – scaling our higher-than-usual cash positions into attractively valued U. S. and foreign equities and alternative assets. Selling will continue in the shortest-term Treasury securities, which have been inflated in price by the global flight to quality. Generic fixed income investment holdings will continue to be minimal, preferring the bar bell portfolio described above to capitalize on the expected gradually improving market environment.

Economy – The global downturn will continue, and is likely to worsen through 2009 and possibly much longer as governments and financial institutions worldwide attempt to limit its severity at the expense of extending its duration. U. S. unemployment will rise well above 7% and production will decline markedly as businesses attempt to align their output with shrinking demand.

Inflation – The widespread actions of governments and financial institutions to support over-extended borrowers with additional borrowings will eventually foster inflation. But, through 2009 at least, it will be moderated by the deflationary effects of the downturn.

Bond markets – Fixed income investors will be increasingly tempted by these government and corporate actions to focus not on the financial health and economic prospects of issuers, but on their perceived economic importance and political strength. It will encourage increased risk-taking by sophisticated, unregulated investors, while driving other investors further into the lowest risk, lowest potential return investments.

Global stock markets – Equities will remain extremely volatile as investors’ hopes for economic recovery are periodically inflated then dashed by economic reports, geopolitical events, and governmental actions. We expect disappointments and new areas of concern to exceed positive surprises, leading to further stock market declines before year-end.

Real Estate – Weakness will moderate in both commercial and residential markets as governmental efforts to increase demand and dampen the growing supply of properties for sale.

Energy and Materials – Efforts by producing nations to curtail output will put a floor under prices, but will be insufficient to push prices sharply higher in the face of continued recession-related declines in global demand this year.

Agricultural commodities – Demand growth in developing economies will continue to support prices in all areas other than current biofuel crops where the accelerating development of alternative biofuel sources is likely to depress prices.

Precious Metals – Weakness in industrial demand will be more than offset by investors’ increasing desire for safe, universally honored, “hard” assets.

Currencies – Efforts by investors and commercial users of the currency markets to discern the relative prospects for the G8 and developing economies will keep these markets volatile week-to-week and month-to-month, but largely trendless from the beginning to the end of 2009. We believe the U.S. Dollar will remain stable during the global crisis and economic downturn. The Dollar remains the reserve currency of choice for now.

External Market Influences – Difficult economic conditions around the globe coupled with a new administration in Washington and a plethora of geopolitical confrontations are certain to produce worrisome incidents throughout the year. Investment markets will react accordingly, with risk premiums remaining high and the lowest risk investments moving to even higher valuations.

Our Recommendations:

Diversification, which provided only limited protection in 2008, will be more important in 2009. We expect the greatest success with “bar bell” allocations – those consisting primarily of some very safe, highly liquid investments together with a modest but growing exposure to carefully selected higher risk assets. This mix, if well managed, should provide returns significantly in excess of a portfolio of all asset classes equally weighted.

Trading will become more important in the volatile but range-bound markets we expect. Buy-and-hold returns in most asset classes will be largely disappointing.

Patience will be required throughout the year, although limited market rallies will provide occasional encouragement.

Volatile but generally trendless markets (as described) appear most likely, but the precarious nature of global economies and geopolitics creates the possibility of sudden large moves in either direction reaching extreme levels that could persist for an extended period. So, although we never expect to fully capture any such surprise moves, we will remain vigilant and ready to reallocate our portfolios as we deem prudent in response to the expected rapidly changing environment.

CoreStates Strategies:

The best long-term investment purchases are made when others are selling, when fear is greatest, when the outlook is most bleak. The current environment certainly fits this description. But, we expect this gloom to gradually (though erratically) dissipate over the next several quarters. We intend to capitalize on this by carefully managing but generally retaining our current allocations, but also doing some strategic buying – scaling our higher-than-usual cash positions into attractively valued U. S. and foreign equities and alternative assets. Selling will continue in the shortest-term Treasury securities, which have been inflated in price by the global flight to quality. Generic fixed income investment holdings will continue to be minimal, preferring the bar bell portfolio described above to capitalize on the expected gradually improving market environment.

Subscribe to:

Posts (Atom)