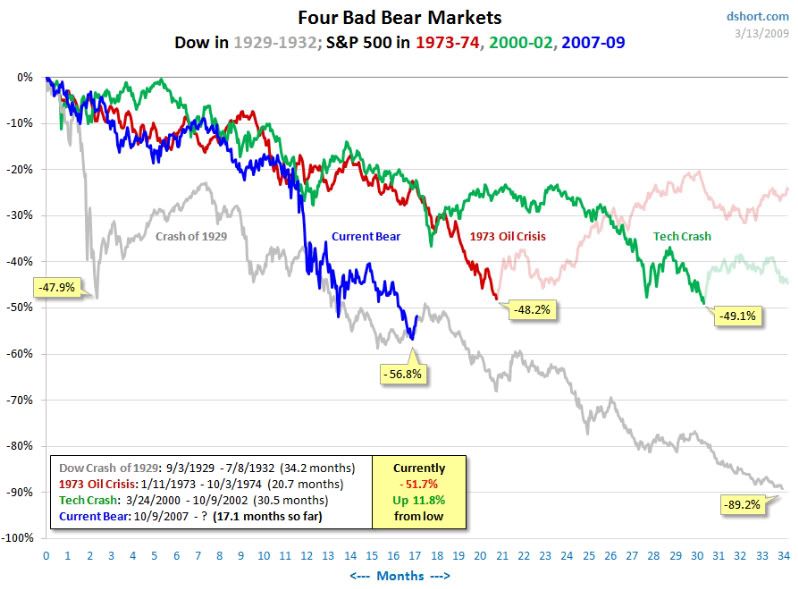

Never before in the post-war era have U. S. investors had to deal with a crippled financial system, such monumental depth and breadth of change, and a pervasive uncertainty about the future. And, never in any modern era have we had to do so while also experiencing the waning of our nation’s global economic power, international prestige, and internal potential for future growth.

Even more importantly, never before have U. S. investors had to deal with the kind of investment markets produced by this new economic environment – investment markets that lack the underpinnings of a consistently growing and increasingly productive economic base. In this previously unknown environment, most investors will be essentially investing blind.

The reasons behind the gradual dissipation of the foundational substance of our nation and economy are many, varied, and controversial. So, I will leave the explanations and evaluations of the causes (e. g., the opinions) to the political pundits and economic editorialists.

The more important issue is this: What can investors do to protect their lifestyles and preserve their economic legacies in this extremely hostile financial environment?

At CoreStates Capital Advisors, we have been pondering this question since well before the severe market erosion began. Our approaches will continue to develop and evolve, of course, but the following are some of the key concepts, strategies and tactics we have been implementing for our clients in our pursuit of investment success in this new environment.

21st Century Diversification

The four-cylinder portfolios (stocks, bonds real estate and cash) of the 1980s gave way to the eight cylinders (adding energy, precious metals, commodities and currencies) of the 1990s, but success in the 21st century will require all of this, plus the ability to be long or short in each category, and with manager discretion within each of the categories to move among style boxes, or even to abandon the style box concept for a more opportunistic approach.

Emphasis on Liquidity

An investment’s returns become “real” only when the investment is sold. Until then, they are only on paper. But, when sold, the return is locked in. So, it is critically important never to be forced to sell an investment, especially a highly priced volatile investment, at an inopportune time. The only way to achieve this is by maintaining enough liquidity in price-stable form or in truly uncorrelated assets to meet any scheduled or unscheduled cash needs.

Dynamic Allocations

The days of fixed allocations . . . never really existed. Going forward, dynamic allocations will become even more important as most markets see their historically upward bias diminish or even reverse, making all markets into trading markets and generously rewarding those investors able to capitalize on their inherently higher volatility.

End of Indexing

The days of buy-and-hold investing are also over. Active security selection will be more important than ever as increasing global competition as well as the mounting geopolitical challenges make the generation of corporate earnings increasingly difficult. In a flat-to-declining overall economy, “par” corporate performance will be insufficient to provide attractive returns to shareholders or even to maintain long-term credit quality. We must invest accordingly.

Focus on quality and valuation

The easy investment approach for the coming years will be to focus on quality . . . and settle for near-zero nominal returns in a potentially high-inflation environment. True growth of purchasing power will be achieved only by correctly evaluating investment quality and being willing to trade among quality levels based on their current relative valuations.

Polar Portfolio Positioning

Implement all of the above points and you are likely to find yourself with a “polar” portfolio – one consisting primarily of some very high quality, liquid assets and some very cheap, but rather speculative, exposures. Middling opportunities are likely to provide piddling returns as most investors seek to improve on low risk, low return investments by edging up the risk spectrum, thereby bidding up prices and diminishing their returns.

Importance of Judgment

Investing driven by historically based, “black box” models becomes less and less effective as the future becomes less and less like the past. The sea change in our worldwide investment landscape is rendering not only past models ineffective, but weakens the very concept of historically based investment models. The next generation of quantitative market analysis will require a higher level of investor behavior-based sophistication, as well as a very influential overlay of superior investment judgment.

Commitment to Patience

A more volatile, changeable market demands a more resolute, patient investor. Returns are certain to be erratic. Extreme market moves will be more common. Directionless markets will become the norm. Periods of steady, positive returns will be extremely rare.

We at CoreStates have no legacy investment styles that we must maintain. Our product is building client portfolios in whatever way we believe will be most effective in the years ahead. This gives us the freedom to truly serve our clients’ needs as those needs, and the market’s nature, change over time.

To us, this is the only way to do business.